Sustainability discussions are always closed off to a few elite circles, but by democratising sustainability knowledge can we reach everyone out to sustainability.

About the author

Malcolm Wong Jun Xiang is an undergraduate student in Malaysia. All opinions written in this article are solely the writer’s.

Introduction

If you are residing within a hotel within the bustling highways of Kuala Lumpur; there happens to be a peak hour when e-hailers and private chauffeurs gather in one spot, that’s when you know for sure a conference is happening within their venue. They can be identified by their business attire carrying backpacks and blazer suits.

No, they are not here for vacation, contrary to the atmosphere of relaxation fueled by refreshments of bottomless latte and food catering of Malaysian cuisine may imply. All are here to talk business. At least, only a select few. The few selected speakers get seats on stage and microphones regularly.

Pay attention and you may listen to the key words by ESG, Sustainability, and maybe social obligations. In more recent summits held after July 2023, you may hear that “The era of global boiling has arrived,” says UN Chief Antonio Guterres. Anyone hearing the provocative statement may experience a brief state of shock, but urgency resides back to normal.

As soon as the conference ends or is in intermission, more often the networking happens, less so on the exchange and retainment of ideas. Big and ambitious ideas of sustainable practices and change management happen to be common values bringing everyone together and networking with other like-minders.

Exploration of Values brought them together, yet the values are not retained. Often people come out with fewer ideas than a longer list of contacts. That phenomenon is not unsurprising nor heartless by all present. These behaviors can only come from discussing climate change in a hall capable of hosting up to hundreds of people seated comfortably with air conditioning, all dressed in business attire.

I bring up Conway’s Law in this context: that events organized meant for the business community are the results of their own communication systems and networks. As conferences are primarily intended as platforms for industry engagement, these sustainability summits by design of the event itinerary become spaces of reflection of the professional community itself.

Climate Change is treated as a Business Opportunity, not as an ethical duty

Per my observations, most participants of climate/sustainability summits happen to be managers of the professional industry from financial services, training providers, or e-commerce. There is the occasional undergraduate or pre-U student privileged enough to obtain an invitation to chat with who could possibly be their potential employer.

No doubt the one drive our passionate attendees have in common regardless of who they are is to make deals of some sort in the brief void of space and time. Look around, your mind will rack up some faces worth talking to. They’re big players, well-connected people in the industry, and certainly worth having a chit-chat with, right? If anyone has any innovative ideas, no one would be a fool to share them with anyone, except for an elevator pitch.

Rarely I have seen or heard any discussions on ideas shared on the subject issue outside of the hall. All are looking for connections, not solutions. And here we have our premier flaw; climate change is viewed as a profitable opportunity, never as a duty to mitigate. Environmental ramifications are treated as side effects to be mitigated lest they threaten the long-term profitability of the business.

Do not assume that more conferences are held on climate agendas, which means that more actions will be taken. By its present design, only more deals will be made, and many more business cards passed around.

This problem is not just inherent in the private sector. When our Prime Minister and Minister of Economy announced ambitious plans such as the Energy Transition Plan barely gained any traction and the Budget 2024 tabling barely gained any momentum outside professional circles. Readers gloss it over as just another mundane news.

While the whole nation knows about the numerous political scandals the day it happened. Does the public care about gossip? Yes, they love outrageous news, but only because they are not in a position to be involved in productive discussions.

Big plans are too detached from the working layman because they are always excluded from debate. What happens if they try to enter a sustainability summit? Only a few people at the top speak, and the rest follow and agree. It is also not that likely that you will get meaningful conversations unless they are connected by career descriptions have known each other before, or are in a similar network of professionals. The flow of knowledge is closed off to a restricted circle.

Exclusion is a matter of priority, never an evil conscious effort. Corporate Boards want action fitting in with the latest trends of net zero carbon and renewable energy, without knowing how. That decision is left up to the upper or middle management, (sometimes the engineers) unfortunately, saddled with the burden of executing and guiding company policy on sustainability from scratch at the same time.

Look into any Publicly Listed Company’s annual report, and you are treated with figures, charts, and incentives listed – all racking up hundreds of pages – each to signal their determination and commitment to social responsibility in ESG to the Board of Directors and Shareholders. Facts and figures in minimalist colorful charts are showcased, accompanied by explanations tied into sustainability keywords.

Nothing wrong with these new trends, but let me pose a question: How many adopt ESG frameworks out of their sincerity to do good and give back, rather than out of a compliance necessity?

As a trend every firm is chasing, most sustainability incentives are structured around meeting ESG requirements (each differs depending on the frameworks and compliance) The SDGs are flocked around as a reference, but a lot have not worked beyond the concept framework to see how it matters, and if it really is beneficial for the community.

If the climate agenda is primarily shaped by professionals with metrics and reports, there will no doubt be demand for said ‘skills’, meaning a higher salary with greater benefits. With the utmost priority on meeting indicators, Malaysia could only produce experts to measure them, not actually develop the skills needed to innovate technological solutions to combat climate change.

What firms can’t do – or talk about

Present rhetoric on Mitigating Climate change has led us to believe that our key direction is to preserve current conditions, deemed optimal for operations: Consume less while producing more value, but less so on cleaning up the damage.

Climate change is neither our only threat, but just one of several manifestations. Business professionals are silent on Microplastic pollution as a potentially threatening major health crisis, and it does not go beyond simple discussions because researchers are not there to advise everyone.

Provided the treasury is filled with enough monetary resources, you can afford to hear from consultants behind closed doors, the rest of the community is blocked off from listening by financial barriers. And the firms with a larger valuation stand a greater chance of hearing.

It is absurd then to expect small entrepreneurs to worry about the carbon footprint of bread and butter, especially from the scarcity thereof. The people who stand the most to lose from agricultural loss, habitat loss, and deforestation will not wear blazers or dress shirts; rather everyday clothes of t-shirts, shorts, and dresses.

Changing the Flow of Discussion

Everyone stresses the need for a change in mindset to address in climate crisis, but change requires creating favorable conditions for new ideas to flourish without much obstruction and any avoidance of derailment to deviant malice.

Conferences are a great venue for voices to be heard, by the people in the foreground, running SMEs, agriculture associations, and students, and workers at the very foreground. If we were to generate fruitful discussions, we would have to change our event design.

Let us change our mindsets for a bit. What if we were to not just listen to a selected few from top echelons, but from everyone who has sufficient insights no matter their position? If we switch our notions that knowledge is more valuable than connections made. We may perhaps get people from all sides involved in discussions.

Instead of listening to a few keynote speakers, how about we listen to everyone in the room? In my experience, the events with smaller attendance and venue size often have the best interactions and participation rate in sharing and giving their thoughts, and often most do speak up and contribute regularly other than the assigned guides on a subject matter. What they, and all contribute are their experiences and lessons learned for all to share.

Professor Emeritus Tan Sri Dr Zakri Abdul Hamid has noted in one of his commentaries for the New Straits Times: that several research and recommendations gather dust in libraries, even as they are publicly available online.

From the author’s experiences, the ones with the most insightful ideas came from professors with decades of research. They are the ones who do fieldwork and conduct experiments. They have first-hand experience with the consequences and know the science.

And it’s not just the professors either. Conversations must be held with all representatives of stakeholders, be it consumer associations, from the agriculture or construction industry. The engineers who are the forerunners of sustainable technology. All must be in the same room together given the opportunity to contribute their insights.

Should discussions occur in a mass setting where public opinion plays a role in the physical presence of other stakeholders involved, the inequality of wealth and position will be dissipated, and the chance to speak will be shared by everyone. This is the democratization of knowledge, where information and ideas flow both ways from multiple points and is heard by all.

In a room where few people speak and most people listen, there will always be more questions than answers. There have been eight people with microphones getting heard. It is time for hundreds more to solve problems with shared answers.

Climate Action is never firstly a professional business opportunity, it is first and foremost an ethical and moral duty. Values insert themselves into opportunities, never was it meant to be the opposite. Money accumulates within a minority. Knowledge spreads to the majority.

If we were to meet our zero carbon targets and cap the temperature increase at two degrees by 2030, it would mean democratizing knowledge on climate action and opening the flow of information to all corners of society as a social obligation. Everyone will come out with knowledge from beyond their field, as a collective effort to provide a sustainable society.

Writer: Malcolm Wong Jun Xiang

Designer(s): Abdul Mustakim, Hannah Jasri, Wong Yan Qi

Note: This is an explainer of the current financial trends for purely educational and informative purposes, and is not meant as investment advice.

Introduction

In June 2020, Open-AI finally released Chat-GPT 3, after numerous iterations and significant improvements from the previous models. Despite not being the first within the publicly accessible AI software space, Chat-GPT 3 took the world by storm. Within months, it was integrated into many aspects of our society. Students utilised its advanced natural language processing abilities to assist in essay assignments, e-commerce businesses leveraged on its machine learning capabilities to implement online chatbots, and social media users posted impressive images generated by AI using simple text commands. The release of Chat-GPT 3 was significant as it provided the general public with direct exposure and access to the full capabilities of AI technology unlike any other software before. Since then, investors’ interest in AI and its place in our future has kept up a steady momentum. The results of this can be seen in securities exchanges and markets across the globe, with companies riding on this AI revolution experiencing significant increases in valuation. The question, however, is whether this exponential growth experienced amongst tech companies is sustainable or just a bubble waiting to burst? To answer this question, we must first understand the reason behind why businesses have gravitated towards AI technology and the services it provides.

The AI Wave

The power of AI lies in its ability to take in, process and interpret vast amounts of data in a very short amount of time, far beyond what a human is capable of. Already within the e-commerce space, big names like Amazon, Netflix, Spotify and Apple have been at the forefront of AI use in analysing customer data. For example, Amazon uses AI to analyse customer activity and historical purchases to provide curated product recommendations. Have you ever googled a product and within 5 minutes, been bombarded with Amazon promotions of that same product? Yup, that’s AI at work! Spotify on the other hand employs complex AI algorithms that interpret your recently played songs to make personalised suggestions for music you have yet to listen to. Within the social media space, apps like Tik-Tok, Instagram and Snapchat carefully curate the content you see on your feed based on your interests, as gathered from your previous in-app and even cross-app activity. This is to keep you scrolling and improve overall user retention.

Demand for AI software has also benefited from the increased popularity of self-driving vehicles. With companies like Tesla and Ford configuring it to enable road navigation and traffic, without you needing to so much as touch the steering wheel. As for financial institutions, AI has been seen as a way to improve the accuracy and speed of investment analysis. For instance, hedge funds have learnt to integrate AI into their investment strategies by using it to predict potential stock price changes based on many factors, including economic indicators, geopolitical events and even social media sentiment. This has provided these firms with a competitive edge in predicting market shifts. Essentially, AI technology has been utilised across numerous industries, companies and aspects of running a business. Unsurprisingly, this burst in demand for AI tech has generated great earnings for companies that stand to gain the most from future AI development.

Market Analysis

The large rally experienced by financial markets this year has been primarily driven by the increased enthusiasm in AI development. As shown in figure 1, the IT sector drove approximately two thirds of the S&P 500 performance, an index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States. This growth was led by the 179% return for NVIDIA, 134% return for Meta Platforms, and 109% return for Tesla, all companies that have revealed AI integration as one of its main growth drivers for the coming future. The IT sector has also contributed 76% of the overall 4.79% return year-to-date of the MSCI Emerging Markets Index, an index that tracks mid-cap and large-cap stocks in 25 countries across emerging markets. This was largely due to significant AI component manufacturers and service providers located within the region, such as Taiwan Semiconductor Manufacturing (TSMC) and Tencent.

Figure 1: IT sector contribution to year-to-date returns of index’s

As of 29 June 2023, Source: Lazard Asset Management

Undoubtedly, the tech firm that gained the most, Nvidia, has greatly exceeded expectations by achieving a market capitalization growth of almost 100% in just 9 months and eventually reaching 1 trillion dollars in May. At the core of its business is its specialisation in generative AI, which it has integrated into its service and product line. From GPU hardware, AI driven business solutions, and cloud computing services, Nvidia has become many businesses’ go-to destination for incorporating generative AI into their day-to-day operations.

Certain tech stocks, along with Nvidia, have performed so well recently that they were labelled “the magnificent seven”. Coined by Bank of America analyst Michael Hartnett, this phrase refers to seven tech stocks that have run circles around the benchmark S&P 500 and brought the index into a bull market. These seven stocks consist of Nvidia (semiconductors), Microsoft (software & cloud computing), Amazon (e-commerce & cloud computing), Meta Platforms (social media), Alphabet (Google parent), Apple (iPhones & iPads), and Tesla (electric vehicles & solar power).

Figure 2: Market Capitalization of Nvidia

Source: Macrotrends.net

Figure 3 displays the explosive growth the “magnificent seven” stocks have experienced, with the S&P 500 performance as a benchmark. Analysts have stated that these explosive stocks are the main reason as to why the S&P 500 has been as bullish as it has, despite rising interest rates, tightening consumer spending and market uncertainty.

Figure 3: Year-to-date returns of the S&P500 and the equally weighted ‘Magnificent Seven’ stocks

Source: Morningstar Direct as of 7/31/23. Equal weighted return takes a simple average of returns of AAPL, MSFT, AMZN, NVDA, GOOGL, TSLA and META.

Elsewhere in the tech sector, SoftBank-owned chip designer Arm, is in the midst of going public with a valuation of $52 billion, making it the largest US initial public offering (IPO) in the last two years. Arm Ltd has greatly benefitted from the AI wave as its main product offerings consist of designs for computer processing units (CPUs) which are the backbone of AI technology today. With a market share of more than 99% and an average gross margin (profit as a percentage of revenue) of 95%, investors are confident that Arm will continue its dominance within the emerging tech sector.

Sustainable Growth or Just Hype?

Amid this recent AI hype amongst investors, there also exists scrutiny on the sustainability of it and whether a severe correction – reminiscent of the dot.com bubble burst in the early 2000s – is in the works. For instance, many experts from Wall Street banks such as UBS and Bank of America, have cautioned investors over overvalued companies that claim to lead the way in optimising AI for growth and profitability. The fear is that these companies are receiving historic valuation increases based on speculation instead of fundamental analysis.This poses an eerie similarity to the period between 1995 and 2000, when investors pumped money into internet-based startups in the hopes that these fledgling companies would soon turn a profit. And when the vast majority of these ventures ultimately fell short, they failed, swallowing roughly $5 trillion in fundraising. However, a notable difference between the recent AI hype and the dot.com bubble is that within the AI industry, the big players comprise of well-established companies with successful track records. In contrast, the dot.com bubble was led by newly-founded startups with no historical performance, and a business model solely reliant on one product. Moreover, these AI related companies are also heavily backed by veteran entrepreneurs from Silicon Valley, such as Elon Musk (Tesla), Tim Cook (Apple) and Sundar Pichai (Google).

Another point of worry is that market concentration along the supply chain, particularly amongst upstream suppliers, pose significant geopolitical risk. As exhibited in figure 4, the foundry market is heavily concentrated. Foundry refers to the process wherein silicon wafers are manufactured. These wafers form the foundation of microchips, which are essential for housing the microscopic and delicate transistors and other miniscule components that power AI. The Taiwan Semiconductor Manufacturing Company boasted a 55.5% market share last year. This places the future of the AI upstream supply under great uncertainty as the US-China tensions continue to grow. With China declaring intentions on invading Taiwan and the Biden administration banning investments in China’s tech sector, the world’s supply of microchips may be at risk.

Figure 4: Top Ten Foundry Companies by Market Cap (2022)

Source: IDC.com

Conclusion

All-in-all, AI development remains a hotly debated topic. Some rejoice at the potential future of innovative consumer products that will make our day-to-day lives more efficient and convenient, whilst others are fearful of the consequences it may bring for traditional occupations that are in danger of AI automation. Nevertheless, it is imperative to ensure balance between embracing the many advantages of AI while addressing its associated disadvantages. Thus, shaping a future where AI enhances human lives ethically and responsibly.

Economic growth, the ultimate goal of nations, is a multifaceted concept that encompasses various indicators like GDP growth, wages, and state revenue. However, at the heart of sustainable growth lies stability, particularly in the realms of prices and currencies. Central banks play a pivotal role in achieving this equilibrium, ensuring that economic growth is not a fleeting occurrence but a sustained phenomenon.

The intricate relationship between stability and growth forms the cornerstone of a robust economic landscape. Stability provides the necessary foundation upon which growth can flourish. Stability, in this context, can be defined as the ability to maintain consistent and predictable economic conditions. This includes maintaining price stability, which prevents hyperinflation or deflation, and currency stability, which safeguards against volatile exchange rates. Price stability ensures that consumers and businesses can make decisions with confidence, while currency stability fosters international trade and investment.

Defining indicators for economic growth and stability entails examining a spectrum of metrics. GDP growth serves as a prominent gauge of economic expansion, reflecting the overall increase in the value of goods and services produced within a country. Alongside GDP, indicators like unemployment rates, wage growth, and consumer spending contribute to a comprehensive understanding of economic health. For stability, the Consumer Price Index (CPI) and exchange rate volatility act as barometers, reflecting the stability of prices and currencies, respectively.

Central banks, such as the Bank Negara Malaysia (BNM), assume a crucial role in maintaining economic equilibrium. Central banks are responsible for formulating and implementing monetary policy. They adjust interest rates, manage the money supply, and use other policy tools to influence borrowing costs, control inflation, and promote economic growth. By effectively managing monetary policy, central banks can support stable prices, encourage investment and consumption, and foster overall economic stability. Central banks have a key role in regulating and supervising financial institutions. They establish and enforce prudential regulations, conduct inspections, and monitor the financial system to ensure its stability and integrity. Through effective regulation and supervision, central banks contribute to the prevention of financial crises and the maintenance of a robust banking sector.

As regulatory authorities, they wield various tools to influence economic activity. These tools include open market operations, where central banks buy or sell government securities to influence the money supply; interest rate adjustments, which impact borrowing costs; and reserve requirements, which control the amount of funds banks must hold in reserves. The BNM, for instance, leveraged these tools during times of crisis, such as the COVID-19 pandemic and the 1Malaysia Development Berhad (1MDB) scandal, to stabilise the economy and restore investor confidence.

The concept of a free market, while facilitating competition and innovation, can sometimes lead to market failures and economic instability. The global financial crisis of 2008 starkly exemplified the perils of a laissez-faire approach. Regulations, as wielded by central banks, act as guardrails, preventing the excesses that can destabilise economies. In Malaysia’s context, the BNM’s intervention during the 1997 Asian financial crisis underscores the importance of regulation in preventing economic collapse. By enacting prudent measures and supervising financial institutions, central banks can moderate extreme market fluctuations.

Central bank independence, the principle that central banks should operate free from political interference, is integral to their effectiveness. An independent central bank can focus on long-term economic goals rather than short-term political gains. Malaysia’s case makes a compelling argument for central bank independence. When the BNM’s autonomy was eroded during the 1980s and 1990s, it led to misguided policies that contributed to the Asian financial crisis. Conversely, when the BNM regained independence, it was better equipped to navigate subsequent crises.

Malaysia’s economic landscape is heavily dependent on international trade and investment. As such, an open economy is desirable to ensure sustained growth. However, this openness exposes the nation to external shocks and exchange rate volatility. The BNM can tailor its regulations to strike a balance between attracting foreign investment and safeguarding against vulnerabilities. By implementing robust financial regulations and maintaining currency stability, the BNM can nurture an environment conducive to growth while mitigating risks.

In shaping policies for the future, the BNM should prioritise maintaining price and currency stability while fostering an environment conducive to investment and innovation. Continuous reforms should be pursued to enhance regulatory frameworks and align with evolving economic dynamics. While the degree of reform should be balanced to prevent undue disruption, the overarching goal should be to ensure that the BNM remains a stalwart guardian of Malaysia’s economic stability and growth. While independence grants central banks the authority to make policy decisions, it is important that they are transparent and accountable for their actions. Independent central banks often have a legal obligation to provide regular reports on their activities, explain their policy decisions, and be accountable to the public and relevant stakeholders. This transparency enhances public trust in the central bank and ensures that the decision-making process is conducted in a responsible and accountable manner.

In conclusion, the intertwined nature of stability and growth forms the bedrock of a thriving economy. Central banks, exemplified by the BNM, wield essential tools to foster stability and regulate the free market’s potential excesses. Central bank independence emerges as a linchpin in this process, enabling long-term economic strategies and prudent decision-making. Malaysia’s experience underscores the significance of this autonomy. As the nation navigates an open economy, the BNM’s ability to adapt regulations becomes paramount. Striking the right balance will ensure a future characterised by both stability and growth.

BNM Regulating the Markets:

In vying for stability, BNM wields a diverse set of tools and strategies to regulate financial markets effectively.

The first category of tools at BNM’s disposal encompasses monetary policy instruments. Open market operations enable BNM to influence the money supply by buying or selling government securities. Purchasing securities injects money into the system, reducing interest rates and stimulating economic activity. The central bank can adjust key interest rates, such as the policy rate, which has the power to encourage borrowing and investment when lowered or cool down an overheated economy when raised. Interest rate adjustments serve as a regulatory tool by controlling inflation and preventing excessive risk-taking. Lower rates encourage economic growth but may also lead to overheating and speculative behaviour. Conversely, raising rates can cool down an overheated market and curb inflation.Furthermore, BNM sets reserve requirements for banks, controlling the amount of money available for lending. Lowering these requirements provides banks with more funds to lend to consumers and businesses, fostering economic growth.By adjusting reserve requirements, BNM can regulate the money supply and credit availability in the market. Lowering these requirements can stimulate economic activity and investment, while raising them can help prevent excessive lending and maintain financial stability.

The second category of tools involves regulatory measures. BNM formulates and enforces prudential regulations to ensure the soundness and stability of financial institutions. Capital adequacy requirements are a prime example, mitigating risks within the financial system. Moreover, BNM conducts inspections and closely monitors the financial landscape to identify potential issues and risks proactively. Prudential regulations set the standards and requirements for financial institutions, ensuring they maintain sufficient capital and risk management practices. This mitigates the risk of insolvency and instability within these institutions. It also helps maintain market integrity and ensures that financial institutions are conducting their operations responsibly.

In essence, market regulation by BNM means creating an environment in which financial markets operate efficiently, transparently, and with minimal risk. Central banks, due to their authority over monetary policy and their role as regulators, are uniquely positioned to achieve this objective. By employing these specific tools, BNM can influence market dynamics, encourage responsible behaviour, and mitigate excessive risk-taking, ultimately ensuring that Malaysia’s financial markets contribute to both economic stability and growth.

Researcher(s): Pravin Periasamy

Reviewer(s): Malcolm Wong

Designer(s): Azir Irfan, Nabil Jaimey, Tan Yi Pei

References:

(1995). “5 Central Bank Independence and Coordination of Monetary Policy and Public Debt Management”. In Policies for Growth. USA: International Monetary Fund. Retrieved Aug 30, 2023, from https://doi.org/10.5089/9781557755179.071.ch005

Debt, in and of itself, is a scary idea. It implies that something is ‘owed’ and that you are tied down to obligations. You could be in debt to a bank, having taken out a loan to purchase a house, because how many of us can actually afford to buy a house in cash?

But, one should not be overly fearful of debt. In this article, we explore the differences between ‘good’ and ‘bad’ debt, as good debt can help you on your journey to financial independence!

Good Debt

Good debt has the ability to generate money for a person and help build their wealth. This can improve a person’s quality of life in tremendous ways since good debts are considered as investments into one’s future. For instance, when the economy is prospering, the money spent on a university degree can often pay for itself within a few years after individuals join the workforce.

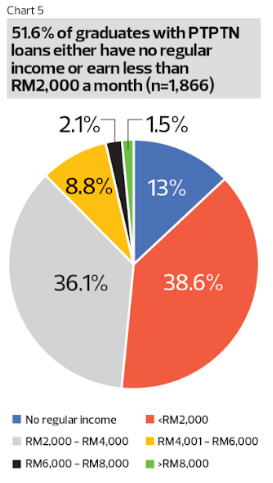

According to the UK government (2019), better-educated people are more likely to be hired for high-paying jobs and are better equipped to find new ones if they need to. However, not all degrees are of equal value. Thus, it’s also important to think about both the short and long-term prospects of any field of study you might be considering. A good rule of thumb is to not borrow more than 1.5 times your first year’s salary for your university degree (Maldonado, 2020).Otherwise, you may not be able to meet the interest debt payments, thus turning good debt into bad debt. On the bright side, there are schemes like PTPTN, which are available to help students from lower-income families pay back their loans over a longer period of time. Thus, children from B40 or M40 families stand a chance to become more educated and find better-paying jobs, without the burden of having to pay back loans immediately. It’s also worth noting that good grades from a prestigious university and stellar extracurricular records aren’t the only determining factors as to whether an individual is able to pay back their student loans. Many factors come into play, but all in all, the loans provide a stepping stone to a brighter future, if one is prudent and cautious.

Another example of good debt would be mortgage loans. Mortgagesare financial agreements, or loans, that allow individuals to borrow from a bank or other institutions to purchase a house or property. Although the interest in taking out a mortgage might be high in the long run, it is imperative to understand that real estate prices tend to appreciate as time passes. When deciding to sell the property, a person typically makes a sum of profit from selling it.

To illustrate this with another example:

If a house buyer in KL were to pay RM1,500 in mortgage payments each month, but were to rent out their house for RM2,000 each month, they would gain a profit of RM500 per month.

Even if the rental market isn’t looking good, first-time homeowners may opt for house sharing with other tenants to generate additional income to pay off their mortgage payments. This way, even if their rental income is less than their mortgage payments, the amount that would have been needed to rent a place elsewhere can be saved (ie. RM2,000).

An additional benefit of mortgage loans is the freedom of having ownership of the property, alongside a number of tax benefits that renters do not get to enjoy in certain countries, like the US (Majaski, 2022). Furthermore, when budgeted prudently, purchasing more real estate and renting them out owned would lead to a stream of passive income. However, it is worth noting that Malaysian homeowners do not enjoy tax deductions on owning their properties and are taxed on rental income.

This applies similarly to business loans. Hence, before taking on any debt, it is always wise to carefully consider what return is expected. For instance, knowing the amount of student loan payments after graduation can help one figure out if they can afford to work in their chosen field and pay off the loan within an acceptable amount of time, or if they should change their major, or choose a more affordable university.

Bad Debt

What is bad debt? Bad debt usually refers to debts that negatively impact the financial well-being of the borrower. Did you know that according to the Malaysian Department of Insolvency, there are 269,654 bankruptcy cases in Malaysia, as of December 2022? These bankruptcies are usually caused by bad debts, of which 42% are caused by personal loans, while 14% are from car loans. Fortunately, bankruptcy rates have been declining, as more Malaysians become more self aware of their finances. Nevertheless, young adults should stay away from bad debts, as we will discuss below.

The main culprit here are personal loans. You can get personal loans from banks and licensed money lenders (note: not Ah Longs). In Malaysia, the maximum interest rate for personal loans is not fixed by law, but it is generally capped at 18% per annum by most financial institutions. However, it is usually advertised at 1.5% per month, in order to entice you with a less scary figure. Imagine if you want to buy the latest iPhone 14 now, and you borrowed RM4,000 in personal loans to afford it, you would have to pay an extra RM720 in interest at the end of the year.

Besides that, car loans are also bad debts in most cases. A car is a personal vehicle you might use to get from A to B, but it quickly depreciates and loses roughly half of its value at the 5-year mark. Therefore, a car loan, or otherwise known as hire purchase, is an unwise financial decision for youths. Possessing loan debts at a young age could hinder your other financial plans. A car loan could be a good debt, only if you use it to generate profit, such as providing e-hailing services (Grab), or using it for your business. Therefore, you should consider relying on public transport, or get an affordable second hand car if you really need one.

Credit cards are also bad debts. When used responsibly, credit cards can bring many good benefits, such as reward points and cashbacks. Many young fresh graduates get easy access to a card once they hit a monthly salary of RM2,000. However, many young Malaysians use them irresponsibly, and only pay the minimum amount required. This causes the debt to snowball, and leads to irreversible damage to their finances. If you cannot afford to pay the full amount, it is still a good idea to pay as much as you can, and consult with a bank officer to restructure your debt.

Buy now, pay later (BNPL) schemes are all over the internet lately, and many Malaysians are eager to give them a try. Many corporations provide BNPL facilities to encourage more spending, such as Grab and Shopee. However, BNPL makes consumers unaware of their financial situation, and induces more spending than they can afford. Similar to credit cards, the late payment rates can cause the debt to skyrocket.

In a nutshell, bad debts are not necessarily bad on their own, but when coupled with bad personal finance knowledge, it could bring catastrophic consequences.

Example: Shopee SPay Later

Before applying for a debt, ask yourself. Can you afford this product and its loan commitments? It may be prudent to take out loans when interest rates are low. After all, this is the intended economic effect of a low-interest environment! Also, do remember that some loans can have ‘variable interest rates’.

To sum it all up, when debt is used well, it can be a great tool for us to leverage our investments and earn more profit. However, when debt is not properly used, it can lead to irreversible consequences that can plague the borrower for years.

Ultimately, it’s crucial to make informed decisions about taking on debt and be responsible with our borrowing habits.

Questions surrounding Malaysia’s National Debt have increasingly become a topic of concern. This, in no small part, has been driven by the recent ‘debt crisis’ in the U.S., where discussions were raised that the U.S. may default on its Debt.

The first time Malaysia’s National Debt gained significant attention was in 2018 when the Pakatan Harapan administration revealed that Malaysia had amassed a National Debt of RM1 trillion. At that time, the ‘Tabung Harapan’ was established, where Malaysians collectively ‘donated’ RM203 million to assist the Malaysian Government in servicing its Debt.

Fast forward a few years later – this sum of RM203 million pales compared to how much the Debt has grown since 2023. As of 2023, Malaysia’s National Debt stands at RM1.5 trillion, according to Anwar Ibrahim, the PMX himself, which represents more than 60% of the debt-to-GDP ratio. When discussing the debt, Anwar Ibrahim emphasises the importance of fiscal prudence. For instance, he notes that wage increases for civil servants will have to be delayed, given that increasing wages will lead to a rise in debt, decreasing investor confidence in Malaysia.

At a glance, this looks troubling. At face value, RM1.5 trillion is a significant amount, which means that assuming there are 31.471 million Malaysian citizens, each Malaysian would owe approximately RM47,662.92. Particularly for the youth, this amount exceeds the average fresh graduate salary and surpasses the savings of many individuals. Given the rise in the debt levels in the past five years, one can assume it will likely continue to increase.

This sets the background for this research piece. Here, we will:

Explore everything you need to know about The National Debt,

Discuss whether you should worry, and

Provide insights into what can be done

But in short, there is no need to press the panic button – you probably won’t have to pay anyone RM47,662.92.

Everything you need to know about The National Debt

The first are the figures as they stand, which are: RM1.2 trillion, and if we include liabilities, the Debt is RM1.5 Trillion.

Looking at the latest data from Bank Negara Malaysia, the Current Liabilities of Central Government Debt amounts to RM1.12 Trillion, and the Debt guaranteed by the Federal Government is RM317.024 billion, totalling approximately RM1.5 trillion. The most pressing question is who this money is owed to.

The reality is that this money is owed to fellow Malaysians. Government debt is not like household debt – when discussing government debt, we are referring to government bonds. By stating that the Debt is owed to fellow Malaysians, we mean that the largest holders of Malaysian government debts are institutions like the Employee Provident Fund (EPF), the Malaysian pension fund. While the latest data could not be found – the best estimate is that as of 2020, Malaysians held roughly 76% of government debt, while foreigners held 24%.

Why are bodies like EPF holding government debt?

Government Debt plays a vital role in financial markets. Another way to think about bonds is that it is a financial security (a tradable asset) that supports the markets. Government bonds, especially those issued by stable governments, are seen as a form of investment that is very low risk and offers a decent return. When we discuss investment opportunities, it may be helpful to think of the risk-reward relationship in the form of a scale where;

On the lowest end: Keeping your money in a bank is extremely secure but yields little return. (The likelihood of you losing money from a bank collapse is extremely low, as banks are typically considered too big to fail and will most likely be bailed out by the Government in times of crisis)

On the highest end: Investing your money in the stock market, where the potential yields could be infinite, but given a company could go bankrupt, has higher risks of losing your money.

A government bond, assuming the country is in sound economic health, is considered a relatively safe investment. Hence, for pension funds on a large scale, these are a great form of investment due to their low risk and decent yield! If the Malaysian Government fails to fulfil its bond payments, you would have much bigger problems than the state owing you money (as seen in the case of Sri Lanka).

Now – we can turn back to The National Debt – and further break down the figures.

Our National Debt is split into two categories: domestic and external. Domestic Debt includes debt and liabilities owed by governments to lenders within the country.

External Debt, on the other hand, refers to the same concept, but the debt is owed to non-residents of the country, which includes private commercial banks, foreign governments, foreign bondholders, or international financial institutions (e.g., IMF).

The National Debt is categorised into short-term debt, medium-term debt and long-term debt.

As of Q1/23, short-term debt is RM43 billion, while medium-term and long-term debt stands at RM1,077.412 billion. Since debts are government bonds, short-term debt refers to bonds that are due to expire and need to be repaid by the Government. This figure is far less daunting than the overall debt figure. If you think about it – if the Government of Malaysia can collect RM1387 in taxes from every Malaysian directly or indirectly, then the short-term obligation can be settled. Federal government revenue in Malaysia in 2022 stood at RM234 billion, so there should be no issue with meeting short-term debt obligations.

The next thing to explore is a concerning figure – the debt-to-GDP ratio.

Per Fitch Ratings, a ratings agency, Malaysia’s debt-to-GDP ratio is projected to grow to 73.3% in 2023, before easing to 72.6% in 2024. At first glance, this seems concerning, and perhaps being so close to 100% is too close for comfort.

But before we dive deeper into the mechanics behind a debt-to-GDP ratio – did you know Singapore has a debt-to-GDP ratio of 168%? This measurement was conducted by the International Monetary Fund, but there isn’t much panic from our neighbouring country to the south. This is because when calculating Singapore’s Net National Debt, the country owes nothing. Net National Debt deducts bonds that the country holds, and the remaining ‘debts’ are mainly kept in Singapore’s banks and serve as a financial instrument supporting the complexities of the financial market. Hence, it may be prudent for the Government to consider the ‘Net National Debt’ – given a large amount of Malaysian Debt is held by Malaysian institutions. If we were to ‘Look East’ again, as we did in the 80’s – Japan has a staggering debt-to-GDP ratio of 227%, but there is little panic about the underlying foundations of the Japanese economy.

Returning to the debt-to-GDP ratio, studies have been conducted, such as the work of Lof and Malinen (2014), which found no robust evidence for a direct impact of Debt on growth in 20 developed countries. Recent studies also argue that it is not a significant cause for concern if countries exceed a debt-to-GDP ratio of 100%. What is more important for emerging markets may be when Debt is held in other currencies instead of their local ones.

If we wanted to explore other numbers surrounding Debt, like the scary ‘Debt Clock, the reality of this number, per economist Stephanie Kelton, is that

“‘The debt clock simply displays a historical record of how many dollars the federal government has added to people’s pockets without subtracting (taxing) them away’”

We’ve illustrated that these numbers should not be taken at face value. Theory and reality often diverge, and as evidenced by the cases of Japan and Singapore, taking a closer look at Malaysian Debt Figures, the RM1.5 trillion figure is less staggering than it initially appears.

However, this does not mean ‘The National Debt’ doesn’t matter. Arguably, the more important thing is this – good fiscal management to ensure the Debt does not balloon.

One of the best examples of this is the 1MDB scandal, and while many are exhausted by the discussion surrounding the Sovereign wealth fund, it is worth repeating as an example of ‘Bad Debt.’ Bonds were raised with very little in productive spending, and given these are bonds guaranteed by the Malaysian Government, they must be repaid.

Ideally, a government bond should be successful if the Government raises RM300 to invest in something that generates a value of RM1000. Not only does this cover the bond repayment and interest, but also effectively reduces the daunting debt-to-GDP ratio.’

We can, however, move on from 1MDB – despite its magnitude and importance – to highlight other aspects of the Malaysian political economy that can illustrate why fiscal prudence is essential.

The Littoral Combat Ship scandal, unearthed by The Centre to Combat Corruption and Cronyism, arguably shows how contracts can be awarded to political allies. Not only are government resources being used for ‘extractive rent-seeking purposes,’ but the disproportionate costs will consequently result in inefficiencies and wastage of public funds.

Another topic worth discussing is ‘Off Budget Projects’ that seems part and parcel of the Political Economy. Projects like MRT1, MRT2, MRT3, ECRL, and 1MDB were made on an “off-budget” basis, meaning that budgets did not go through the process of deliberation and approval in Parliament. Efforts to prevent leakages have been undertaken by the Anwar government, including budget revisions for the MRT3 project.

The key point to illustrate is ultimately, tighter fiscal spending focused on productivity is more important than just implementing ‘budget cuts across the board.’

Namely, spending should be productive: used in a way that generates investments and covers the cost of raising bonds. Increasing fiscal oversight to ensure accountability is key. Government contracts and associated spending should be closely scrutinised. Policymakers should be held accountable to reduce any instances of ‘skimming off the top,’ namely by businesses who may see ‘government contracts’ as an opportunity for ‘rent-seeking’. There is a fine line to walk, as excessive project oversight (e.g., scrutinising and nit-picking on every funding stage of a project) may create excessive red tape that hinders project progression. An extreme example would be needing deliberation on the cost of printing materials in Parliament.

In sum, simply focusing on the figure of the national debt and cutting spending may be short-sighted. Malaysia faces a middle-income trap, with many individuals stuck in low-skilled work, and the underlying infrastructure issues are well-known. More productive spending, coupled with expanding the tax base to include those who currently do not pay, may be a way for Malaysia to prosper in the coming years.

Could Malaysia go bankrupt?

Probably not, given our debt is largely denominated in our own currency, and our ‘creditors’ are Malaysians.

Countries that have experienced debt crises, like Sri Lanka and Argentina, have their debts denominated in U.S dollars and are largely held by foreign funds – which don’t necessarily have the best interest of countries in mind.

But if we were to explore how Malaysia could go bankrupt

We’d begin to default on our debts and monetary obligations (such as subsidies and salary payments).

Credit rating agencies would downgrade our ‘ratings’ at the international level, effectively blacklisting the nation.

This would signal international investors to withdraw their money in fear of losing it all.

We could default if;

Uncontrolled spending on low-return projects

Low-return government projects are generally considered as infrastructure, monetary incentives or subsidies that do not adequately stimulate the economy to grow. For example, imagine spending millions to build a primary school in a retirement village.

The costs of funding and maintenance accumulate over the years, diverting away significant portions of funds that could have been used for more productive projects or incentives to boost economic development.

Excessive embezzlement of funds through corruption.

Missing amounts resulting from embezzlement by corrupt officials (civil servants, politicians), from top to bottom, has to be written off as a loss of funds if the government is unable to track and recover the embezzled funds.

The 1MDB scandal added approximately USD 51.11 billion to Malaysia’s debt, as the embezzled funds have yet to be recovered by the government. Should the amount of money lost to corruption be much higher, the accumulated debt will become increasingly unserviceable.

Lack of reliable government revenue

Government debts cannot be paid if there is no reliable source of income either from taxes, dividends from state-owned enterprises, or interest payments received as creditors.

The question of “What can I do about the rising national debt” can be surmised with:

Pay your taxes.

Keep a watchful eye (or ask your elected representatives) to closely scrutinise all forms of public spending.

Researcher(s): Muhammad Bahari, Seow E Kin Zane Ryan Kate Ng Jia Yi, Foo Siew Jack, Malcolm Wong

Reviewer(s) & Editors: Angellina Choo

References

Bank Negara Malaysia. (2023, June 27). National Summary Data Page for Malaysia. Bank Negara Malaysia

C4 Centre. (2022, September 21st). The Littoral Combat Ship (LCS) scandal – the crooks and villians behind Malaysia’s defence procurement laid bare. C4 Centre

Chester Tay. (2023, Feburary 24th). Fed govt debt likely to rise to 62% of GDP by end-2023 on higher borrowings to fund 12MP, 1MDB bond redemption. The Edge Malaysia

Dr. Temjenmeren Ao. (2021, September 7th). The Political Change in Malaysia and its Economic Implications. Indian Council of World Affairs

Fitch Ratings. (2023, March 9th). Rating Report Malaysia. Fitch Ratings

Investopedia. (2023, May 25). National Debt: Definition, Impact, Key Drivers. Investopedia

Matthijs Lof and Tuomas Malinen. (2014). Does sovereign debt weaken economic growth? A panel VAR analysis. Economics Letters

Rex Tan. (2023, February 24th). Budget 2023: Putrajaya to revise MRT3 project costs, with lower RM45b estimate. MalayMail

Rosli Khan. (2022, August 21st). Is there a need for MRT3?. FreeMalaysiaToday

Stephanie Kelton (2021, January 24th). The Deficit Myth : Modern Monetary Theory and the Birth of the People’s Economy.

Su Wei Ho. (2021, May 21). 6 interesting facts about our government debt. Free Malaysia Today

Teoh Pei Ying, Farah Adilla. (2023, January 17). Malaysia’s national debt now at RM1.5 trillion, or over 80pct of GDP. New Straits Times

The governor of Bank Negara Malaysia (BNM), Tan Sri Nor Shamsiah Mohd Yunus claimed that Malaysia is unlikely to go into a financial recession this year. Does this still stand true in light of the US banking turmoil that led to the second and third-largest bank failures in all of US history? Will there be spillovers and will it have a domino effect on Malaysia? The timing could not have been better as we recently interviewed Firdaos Rosli, Bank Islam’s Chief Economist, right before the recent collapse of the Silicon Valley Bank and Signature Bank. Firdaos has over a decade of experience in the industry, especially during the major financial crisis that Malaysia faced.

Introduction

A typical day in the life of the Chief Economist of Bank Islam is usually hectic, starting with Firdaos reading the current news alongside the latest microeconomics data. He mostly focuses on inflation in the US, which will subsequently fit into the interest rates, unemployment and oil prices policy responses of other parts of the world . Later in the day, he is usually occupied with responding to emails, queries from the media and having meetings and discussions with his staff.

Bank Islam is the only standalone Islamic Bank in Malaysia, thus offering a variety of Islamic products such as stock broking, bank assurance/insurance and unit trust. The three main differences between an Islamic bank and a conventional bank in Malaysia is the concept of riba (anything that is deemed as excessive), maysir (the acquisition of wealth by chance) and gharar (speculative trading).

A Dive into Financial Crises

A “crisis” occurs when “things that are usually within our control go out of our control, and is usually defined by the relevant authorities,” Firdaos clarifies. For example, financial crises are commonly declared by banks and not governments. However, some situations may appear to be crises but are not actually considered as one, so long as things are within control. “For example, this happened last year when the whole world talked about global inflation. However, in the case of Malaysia, it was not entirely a crisis because we were able to mitigate the impact through price controls, subsidies and et cetera,” explains Firdaos.

There are several types of financial crises – currency crises relating to the balance of payments, debt crises, and confidence crises. An example of a confidence crisis domestically was the share prices of MyEG, which went down twice following government announcements and wiping out almost two billion worth of its market value within a week. Firdaos explains that often these crises lead to domino effects. “For example, when Malaysia was confronted with the Asian financial crisis back in the late 90s, it didn’t even happen in Malaysia but it started from our neighbouring countries and spilled over to our banking sector. And then, because of the banking sector, the domino effect was felt throughout other sectors, even those unrelated to banking.”

“Crises usually happen when we are not able to anticipate changes, especially now when things change quite rapidly.” Firdaos notes that, in the past, the time period between one crisis to another was very forgiving, and allowed nations to regain their composure. However, in recent times, crises have been occurring more and more frequently. In the case of Malaysia, we faced the COVID-19 pandemic recently, and prior to that, we faced a drop in global oil prices, falling from 103 USD per barrel to 30 USD per barrel. Fortunately, the fall in global oil prices did not lead to a contraction in Malaysia’s GDP, primarily because GST served as a buffer.

Financial Crisis and Recession, National vs Global?

“A crisis will usually lead to a recession, but a recession is not necessarily caused by a financial crisis,” clarifies Firdaos. “A recession can stem from other parts or sectors that are not financial, but if there is a financial crisis it will surely lead to a recession.”

Several economies have suggested that 2023 will be a recessionary year, as global growth spirals downward, raising concerns. However, the world is incredibly interconnected in today’s age. Although the Western economies – most notably the US and the Eurozone – are going to experience a moderation in growth, China has reopened their economy. This will likely be the engine of growth for the world in 2023, and may even come to balance out the effects of the potential global recession.

Tax policies have also proven to be a saviour for our Malaysian economy. For example, implementing distributive justice, which refers to the distribution of wealth in an economy to be socially fair. GST and SST have also served as reliable buffers for the Malaysian economy. When asked about the key differences between GST and SST and how it affected our economy, Firdaos explained, “SST is a single-stage taxation, or a single-stage consumption tax, which means it is taxed at final consumption. Whereas the GST is multi-layered, so it is taxed at each and every level of value creation.”

“Secondly, SST is a positive list consumption tax. This means that only the goods that are listed in the act are considered taxable. However, it is the reverse for GST – goods that are in the list are not subject to GST, and everything else is subject to the GST rate. The latter would mean that if there are any new technologies or new types of transactions, they will also be subject to taxation.”

This amounts to a big difference in the final revenue gained from these taxes, both serving as useful buffers for the economy in times of recession and crises, depending on how severe the recession may be.

Common Signs and Prevention of a Crisis

Firdaos states that the most common telltale evidence of an upcoming recession is “For Closure” sign boards – outside shops, real estate, and office blocks. However, things have become far more sophisticated these days, as economic metrics have been tracked religiously over the past decade or so, unlike before. Reading the news and keeping up to date with recent global events will make signs of a recession obvious to any ordinary person.

As a developing economy, most, if not all of Malaysia’s past financial crises were externally induced.

Thus, Malaysian economists will often turn to external news, particularly from the US and the EU.These two countries are significantly correlated with our growth, affecting about 88 to 89 percent of it! As far as trade is concerned though, we are closer to China than any other country. Even the economic crisis caused by the COVID-19 pandemic was externally induced, and not by the virus itself but rather by the Malaysian government following other world governments, to impose lockdowns, thus putting the economy at a standstill.

As for what we can do to mitigate the effects of a financial crisis in our lives or in the total economy, there’s really not much that can be done. “Although we reign policy autonomy in fiscal and monetary policies, there are many things that are not within control,” Firdaos elaborates. “For example, there are three things that are not within our control. The first are the fiscal and monetary policies of other countries, most notably the big economies such as the US, the Eu and China. Secondly, global oil prices, and thirdly is general investor sentiment.” These factors can play a significant role in the effects of a recession in our economy and yet are mostly out of our control.

How should citizens prepare and protect themselves from the effects of a financial crisis?

One thing that you should note is that interest rates around the world are decreasing over time primarily due to the impact of economic crises. Governments tend to pursue counter-cyclical fiscal measures every time there is a crisis. This means that though their debt will increase, the imposition of monetary policy will reduce the debt burden through the reduction of interest rates. This allows governments to take on more debt, acting as a stimulus to put the economy back on track.

In Malaysia, interest rates were once double digits but have gone down over time from 3.5% prior to the pandemic, to 3.25% during the US-China trade war, and finally to a historic low at 1.75% during the pandemic. This was done to provide an accommodative environment for economies to thrive during the crisis.

Malaysians are more concerned about consumption now rather than investment, most notably after the Asian financial crisis. Interest rates have gone down as the government encourages citizens to increase consumption. Surprisingly, the government has not mentioned the unsustainability of this practice, as interest rates going down also means that returns on safe assets such as bonds, EPF, ASB and Tabung Haji will also go down.

It appears that consumption is now cheaper than it was prior to the pandemic. Not only that, but the value of assets has increased as well due to technological advancements. There is more technology involved in producing these goods which means that though prices have gone up, financing has become cheaper due to lower interest rates.

Now that the interest rate has gone down, consumption has risen while savings have dwindled. To put this into context, RM 145 billion worth of our old age savings through EPF were withdrawn during the pandemic as a form of fiscal injection.

The government’s lack of appetite to invest in infrastructure and improve our growth rates in the future means that the private sector including households like ours will also have very little appetite to invest. In the 90s, Malaysia had a plethora of mega projects such as KLIA, Putrajaya, the expansion of PLUS Highway and KLCC, providing many opportunities for private investment. However, now, announced mega projects like the East Coast Rail Link (ECRL) are postponed due to corruption which balloons the cost of the project over time.

Citizens should improve their financial literacy, which is what FLY is all about, in order to protect themselves. Firdous reveals that he usually assumes that interest rates would go up, to foster self-discipline in terms of managing his personal finance. His personal finance advice is that it is always much easier to upgrade your life or your standard of living rather than to downgrade.

Bank Islam’s efforts in combating an upcoming financial crisis

Firdous mentioned that since the Asian financial crisis, banks have been putting a lot of effort into ensuring that financial institutions in Malaysia have a good buffer against economic crises. All in all, financial institutions that are bound to Bank Negara rules will continue to abide by the central bank’s leadership. For example, over the pandemic, Bank Islam provided a moratorium, where customers could choose not to pay, or rather, suspend their debt servicing to the bank without hurting their credit score.

Following the end of the moratorium, Bank Negara pursued Targeted Repayment Assistance (TRA) to assist murals in distress. It is still being continued by some banks including Bank Islam today. So, say a borrower is still being faced with tight financial conditions, they could still come to the bank and request for some relief.

There are various financial levers put in place to ensure financial sustainability in both modification losses and provisions done by banks. During the pandemic, banks issued a moratorium and the TRA, meaning that, generally, profits for banks in that particular fiscal year would have to be affected. Therefore, banks set aside modification loss and some provisions for the future. However, as far as banking ratios are concerned, Bank Islam’s cross-impact financing or the TIF remains one of the industry’s lowest. Firdous claims that bank slumps are bearable especially since Bank Islam is very conservative when it comes to lending.

The severity and mitigation of the medium and long-term effects of the 1997 Asian Financial Crisis

Every crisis presents opportunities and threats for the future.

1. Difficult for our financial system to be a part of the global environment.

During the 1997 Asian financial crisis, which was deemed one of the worst financial crises faced by Malaysia, the capital controls[1] put in place meant that we were able to ensure that our crisis responses were done autonomously without the influence of others, especially the multilateral banks. However, it would also mean that it would be notoriously difficult for our financial system to be part of the global environment.

2. Undervalued ringgit

The Malaysian ringgit has been sliding since the age of the financial crisis. Back then, the ringgit was somewhere around RM 2.40 to a dollar. It fluctuated and on the 5th of November last year, it reached its highest ever recorded in history at RM4.75 to a US dollar.

a. Private Investments have not yet returned to pre-Asian financial crisis levels today.

There are no mega projects compared to in the 90s when there was a race for infrastructure projects.

b. The relationship between debt and growth after the global financial crisis.

Primarily, the concern was that Malaysia accumulated quite a bit of debt as a result of the Global Financial Crisis but growth rates were not interesting enough for investors. The previous government tried to control it through the introduction of GST, subsidy rationalisation and by targeting a balanced budget by 2020. Firdous mentioned that although growth rates did go up over the past decade, they still remain fairly flat at about 4-5%, when the government recommends that it should be at least 6% a year.

During the global financial crisis, the subsidy bills in that fiscal year were around RM 90 billion. We managed to cut the fat a bit over the years but it went up again during the pandemic. Firdous mentions that the average income in Malaysia has gone up to around RM 3,007 and that the income-to-GDP has gone up due to the introduction of minimum wage.

Long-term impacts on Malaysia’s labour market as far as Covid is concerned:

1. Our unemployment rate has yet to return to pre-pandemic levels

Firdous expresses that he is unsure whether the incomes have also gone back to pre-pandemic levels as the government has yet to announce it or conduct the household income survey.

2. The decline in foreign workers coming in

This is not only because they see more opportunities in their home countries but also due to the fact that we have tightened our labour laws which makes it harder for Malaysian companies to source for low-skill, low-wage workers.

Effectiveness of the measures taken by the Malaysian government in response to the 1997 Asian financial crisis

The Chief Economist believes that there are two schools of thoughts here. The first is that capital control was effective. The second is that if the Malaysian government were to resort to the IMF for assistance, we would still be able to crawl out of the crisis during the same period. The only difference between the two measures is that reforms in key ineffective industries and/or institutions were not taken. He claims that we tend to get misguided over what is happening around the world if we do everything on our own and the economy will effectively be derailed away from globalisation.

Putting the economy back on the globalisation track would require undoing many of these activities. Industries would have to increase efficiency, and economic activities would have to be more complex resulting in more enforcement.

After the global financial crisis, the government initiated a new economic model to reverse these damages. Unfortunately, it did not receive a positive response from the public, as the reform space was left for some time. Before the crisis, reforms were executed without political hassle as political capital back then was stronger and done consecutively. The change from agro-based to manufacturing to services was done seamlessly prior to the crisis. However, after leaving the reform space, Malaysia has to catch up, especially with our neighbouring countries. For example, Malaysia was known as the regional automotive manufacturing hub in the 90s. However, after the crisis, Honda and Toyota turned to Thailand instead, to expand their manufacturing capacity. Now, many economies foresee Indonesia as the next manufacturing hub due to its potential in battery manufacturing, which may lead to a healthy EV industry. Manufacturers are now bypassing Malaysia for its neighbours.

“Whether or not we are better at addressing a crisis being away or being closer to the global economy depends on the government, as some would prefer to be away from the global economy to get things going while some feel that the reforms would have to be in line with the global economy. The former, however, would require the need to catch up eventually – Firdaos Rosli”.

Important lessons learnt from past economic crises Malaysia has faced

Firdous believes that an important lesson learnt from the two major financial crises we have faced would be identifying whether or not we are better at addressing a crisis being closer or further away from the world. Apart from that, he believes that we must understand that economic policies must go hand in hand with our political development. This is because, at the end of the day, public policy will be shaped by the political development of the nation itself, whether we like it or not.

“Following Malaysia’s 15th General Elections (GE15), we now have a multi-coalition government instead of having a single coalition government, which means that parties not only need to work among themselves, but with coalitional partners as well. However, whether or not this will stand the test of time is unknown”.

“A good Economist will know which one makes sense and which one doesn’t, but a great Economist will put many non-economic factors together to understand the world better. A good Economist will be able to unpack the economic content in the simplest of terms so that everybody understands what you’re saying. So, if you want to pursue economics, make sure you understand the technical bit of it and then rephrase it in a manner that even your dog would understand. – Firdaos Rosli”.

Glossary:

[1] Capital Controls: any measure taken by a government, central bank, or other regulatory body to limit the flow of foreign capital in and out of the domestic economy. These controls include taxes, tariffs, legislation, volume restrictions, and market-based forces.

Financial technology, often known as fintech, has evolved significantly over the years. Traditional financial institutions have already incorporated technology into their services, while digital firms such as Wise and Coinbase have developed inventive alternatives to our conventional ways. Individuals are also beginning to diversify the way they handle their finances and they are looking for a more tech-savvy alternative in contrast to our conventional banking methods. In fact, the neobanking segment is projected to grow by approximately 18.15% from 2023 to 2027 (Statista, 2021).

Over the years, we’ve seen that Apple is no stranger to disrupting a myriad of industries with their unconventional alternatives, from changing the way we listen to music with their pocket-friendly iPods to revolutionising the desktop industry with the famous Macintosh. Recently, they’ve brought in a fresh new addition to the highly competitive Fintech industry with the launch of the Apple Savings account for Apple Card holders in collaboration with Goldman Sachs, a leading global investment bank. While this isn’t Apple’s first venture into fintech with the introduction of Passbook (now known as Wallet) and Apple Pay in 2014 (Brue, 2023), the high-yield Apple Savings account is definitely the biggest venture yet.

How things kicked off

This unique partnership between two giants in their respective industries kick-started in August 2019 when they introduced the ‘Apple Card’ which combines Apple’s knack for simplicity and seamless ecosystem integration along with Goldman Sachs’ prowess in banking and financial expertise. In fact, the CEO of Goldman Sachs, David Solomon, stated that simplicity, transparency and privacy were the core of developing this disruptive credit card that comes with daily cash back and exclusion of fees (Goldman Sachs, n.d.)

While their partnership has faced some roadblocks over the years, with Goldman Sachs reportedly experiencing a pretax loss of $1.2 billion under its credit cards division (where most were tied to the Apple Card) (Natarajan, 2023), there have been some notable positives recorded by this partnership. They have topped charts in terms of user satisfaction among midsize credit card issuers in 2022 (Apple, 2022), and Apple’s growing influence in the fintech industry is not to be underestimated. Their financial service arm, Apple Pay, is projected to bring in 4 billion USD in revenue, which marks an increase of 988 million USD from 2019.

This move to launch the Apple Savings Account shows that they’ve probably sensed an opportunity to leverage on, with uncertainty growing in the conventional banking industry and relatively low average Annual Percentage Yield (APY) in the United States. With this savings account offering an APY of 4.15%, it’s a rather attractive option for US consumers who want to explore ways to grow their savings further.

Revolutionising Savings

Customers can save their Daily Cash earnings from their Apple Card in this account and earn interest on their savings, where they can easily manage their accounts using the Wallet app on their Apple devices. This comes with no minimum deposit or balance requirements as well as being fee-free. Hence, it is a suitable starter account for Gen-Zs who are just entering the fray of working life.

As stated before, the Apple Savings Account has a high-yield interest rate of 4.15%, which is more than ten times greater than the national savings account average in the United States (Federal Deposit Insurance Corporation, n.d.) while also being significantly higher than those offered by big financial firms such as Bank of America (0.01%). On top of high interest rates, each depositor is protected and insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 thus making this savings account a relatively secure place to store savings. With these high-yield rates, it can be treated as a long-term investment alternative with low risk, as interest (read more on practical saving advice here) is reportedly being compounded daily and deposited on a monthly basis.

With a huge user base of approximately 48.7% of the smartphone market in the United States, Apple already has a huge potential target audience to penetrate – and Apple can leverage its brand love, loyalty and technological expertise to provide innovative solutions. The Apple Savings Account seamlessly integrates into the Apple Wallet, allowing users to easily set up automatic savings options and goal-setting tools. There is also a dashboard feature that provides quick insights into account balance and interest earned over time.

What could this bring to the economy?

While it’s worth noting that the Apple Savings account is only available in the United States at the moment, there will likely be plans to bring this worldwide if success follows.

As stated earlier, this account does not require minimum deposit or balance requirements and is fee-free, which indirectly leads to greater and improved levels of financial inclusion in the economy, especially for groups that may not have access to services offered by traditional financial institutions. With greater financial inclusion, more individuals have access to financial services, leading to an increase in consumption and overall economic activity.

This is further fueled by the ease and convenience of payments supported by Apple Pay. When consumption increases, there are definitely positive impacts on the general economic growth, as higher spending leads to greater demand for goods and services, and businesses will be able to generate more revenue. This would be a long-term narrative as the introduction of Apple Savings accounts will not cause these chain reactions in short periods.

Additionally, if the Apple Savings Account acquires a large number of deposits and continues to offer competitive interest rates, it has the potential to drive inflation. This is because more deposits can lead to higher lending and borrowing, which can lead to higher expenditure and, as a result, higher inflation. In the long term, this can drive the prices of goods up. This is supported by a World Economic Forum study, where high inflation rates in 2022 drove Consumer Price Index up by 7.1%, with items like eggs, margarine and motor fuels experiencing a YoY cost increase (Nov’21 to Nov’22) of more than 40% (Koop, 2023).

Furthermore, the relatively high APY offered in the current state of the US economy will drive up competition in the savings account market. As a result of Apple’s brand reputation and loyal customer base (CIRP studies have shown Apple maintains a 90% loyalty in the past three years), other industry players will have to improve their offerings to retain their customers. This will result in a more competitive market, giving customers more options and encouraging industry innovation and development.