1.0 Introduction

Source: http://cdn.digital-photo-secrets.com/images/elderly-man-outside.jpg

Have you ever pondered upon the following question; what happens when you leave your workplace for the one last time after spending most of your life there? Do you live the rest of your life playing with your grandchildren? Or will you struggle to make ends meet and live in despair every single day? This period of time is what we call the retirement life cycle. Retirement starts as soon as the moment the individual decides to leave the workforce permanently (Investopedia, 2016). In Malaysia, the current minimum statutory retirement age is set at 60, however one can choose to retire earlier or later. With the average life expectancy of Malaysia around 77.4 years and 72.5 years for a female and male individual respectively (Department of Statistics Malaysia, 2015), there is definitely a period of time before you kick the bucket.

2.0 Retirement Planning Defined

Unless you would rather reject a comfortable, legs-up life as a retiree, there must be some sort of plan to guide yourself towards that level of life. This is what we call retirement planning. Planning for your retirement refers to the amount of money that you should plan to save now for your retirement purposes. It is essential to form a retirement plan as early as possible as the wealth pool accumulated will be significantly larger than individuals who start at a later time, thanks to the power of compounding. Sadly, in Malaysia, according to a report by HSBC, only 27% of respondents claim that they are able to clearly understand their long-term finances and merely 13% of respondents feel prepared to retire (HSBC Insurance, 2009). The illiteracy rate of people towards their retirement planning is frightening, which can potentially lead to an uncertain quality of life for majority of individuals at their old ages. (but that’s where we come in!)

3.0 Channels for Retirement Savings

Fortunately, in Malaysia, there are various channels available for individuals who are keen to financially plan their retirement, be it government-owned funds or privately-owned retirement plans.

3.1 Employees Provident Fund (EPF)

The Employees Provident Fund (EPF) is one of the most commonly used channel by Malaysians in general as it is deemed compulsory for employees to deposit funds into EPF1, as well as for employers to contribute a portion on behalf of the employees2. The diagram below shows the dividend rates by EPF for the past 20 years:

Source: Employees Provident Fund (EPF)

EPF guarantees an annual base dividend of 2.5% (EPF, 2016), with higher dividends expected if the economy is good in that particular year. For example, there is a steady increase in EPF annual dividend rates from year 2008 – 2014 as the economy was doing well. Besides, it is considered as the one of the safest channels to deposit your funds as it is regulated under the Ministry of Finance. Though, it was reported that 65% of active EPF contributors has less than RM50,000 in their accounts (Bernama, 2016). Perhaps EPF does not provide enough returns with the petty fixed amount of contributions deposited every month, which brings us to private retirement schemes.

Dividend : Regular payments that are given to you as a percentage of the amount of you and your employer’s’ contribution

¹ 11% of wages/salary regardless of income level.

² 12% of wages/salary for employees receiving wages/salary exceeding RM5000 per month, 13% wages/salary for employees receiving wages/salary below RM5000 per month.

For more information about the EPF, kindly visit the website stated below: http://www.kwsp.gov.my/portal/en/web/kwsp/home

3.2 Private Retirement Schemes (PRS)

Other than government-owned funds, there also exist private retirement schemes offered by various banks’ asset management or mutual funds divisions in Malaysia. These divisions are called Private Retirement Scheme Providers, or PRS Providers.1

The main difference between the EPF and PRS is that PRS offers the flexibility to deposit any amount of money into the scheme every month while EPF deposits a fixed percentage of income into the EPF account. This means that the PRS may potentially offer higher returns if the dividend rates are high and the total funds deposited it large enough. Besides, since the procedures of depositing additional funds into the EPF is tedious,2 people may opt to deposit their funds into PRS to save the hassle.

Though it should be reminded that PRS funds will be dispersed into 2 subaccounts at a 70-30 ratio. If the individual wishes to withdraw money from the PRS, the individual can only withdraw money from the latter account (30% account) (Chan, 2015). Hence, careful consideration of deposits must be made by the individual as funds are not easily withdrawn.

¹ Currently provided by 8 banking groups in Malaysia.

Full list available at: https://ringgitplus.com/en/blog/Budgeting-Saving/A-Guide-to-the-PrivateRetirementScheme-PRS.html

² Requires the individual to fill up a form and apply for it. If there is any changes after that, the individual is required to go through the same procedure again.

3.3 Individual Savings & Investments

In addition to above, one can simply save in whichever bank account, or invest in any investments he or she see fit. However, we will discuss inflation, in which interest rates in banks barely keep up with, as well as the lack of investment knowledge that puts this option at a huge caution.

4.0 Additional Factors to Consider

Of course, there are many more ways to finance an individual’s retirement, but the 3 listed above are some of the common ways to do it. Other than comparing the characteristics, benefits, and disadvantages of each channel, it is important to consider in some external factors as well.

4.1 Inflation

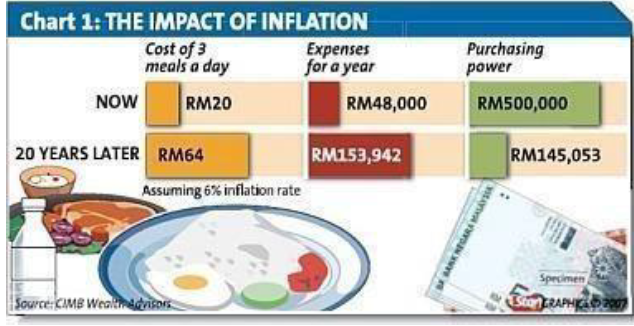

Rise, rise! Except for the value of your money.

Source: The Star Online & CIMB Wealth Advisors

Inflation, an overall general rise in prices of goods (Brealey, et al., 2001), will affect your retirement planning. Constant increases in expenditure per annum is inevitable, causing a shrink in value of money over time. It is important to remember this quote “a dollar today is worth more than a dollar tomorrow” 3. Hence, the total estimated savings should deduct off inflation, giving a real amount4 of it.

3 Simple illustration: You can buy a piece of roti canai for RM1 today, but it might cost more in the future. Perhaps it will be RM2? RM3? We don’t know. But it is certain that it will cost more than RM1 as the value of money has shrunk.

4 Amount of money after deducting inflation.

4.2 Medical Costs

Source: http://www.healthjobsweb.com/images/hospital-medical-tech.jpg

Trust me, medical bills will be presented to you at a more frequent rate than you will have expected at your older ages. Medical costs are also expected to increase by at least 15% per annum (Habib, 2007). In order to not further financially burden your children with your medical bills, it is advisable to get attached to a health insurance5 as soon as possible. Health insurances prevents a heavy depletion of your retirements funds as it covers part of your major medical costs. For example, health insurance subscribers will be compensated some amount of money if they undergo certain surgeries or treatment for certain diseases.

5 Examples of health insurance can be found here: https://ringgitplus.com/en/health-insurance/medical-card/

4.3 Longevity Risk

Longevity risk is the risk that you live too long (what a drag!) such that your funds will have depleted as time went on . As your lifespan is unknown, this makes saving for your future a lot more uncertain as it becomes a lot more difficult to determine the total amount you’d need at retirement. One particular product that transfers this risk to an insurance company is called an annuity. An annuity promises regular payments to you until you die, subject to various increases in payments depending on the insurance company.

5.0 Conclusion

There are limitless personal factors to consider as well. However, the moral of the story is the earlier you plan for your retirement, the larger the funds available for your retirement. This is because you will be able to contribute more to your retirement plan as you are earning income. It was also reported that half of our country’s retirees have depleted their EPF savings within 5 years of withdrawal (Arfudi, 2015), therefore it is advisable to save in multiple channels to meet your financial needs when you are old.

Download the Report and Infographic Here:

[download id=”131″]

[download id=”134″]

[tw-toggle title=”References “]

Arfudi, Z., 2015. Malaysian Digest. [Online]Available at: http://www.malaysiandigest.com/features/585044-50retireesexhausted-their-savings-within-five-years-of-retirement-how-canyouavoid-this.html [Accessed 13 September 2016].

Bernama, 2016. Free Malaysia Today. [Online] Available at: http://www.freemalaysiatoday.com/category/nation/2016/05/15/money-inepf-but-not-enough-for-retirement/ [Accessed 10 September 2016].

Brealey, R. A., Myers, S. C. & Marcus, A. J., 2001. Fundamentals of Corporate Finance. 3rd ed. s.l.:The Mc-Graw Hill Companies.

Chan, D., 2015. RinggitPlus. [Online] Available at: https://ringgitplus.com/en/blog/Budgeting-Saving/A-Guidetothe-Private-Retirement-Scheme-PRS.html [Accessed 12 September 2016].

EPF, 2016. Employees Provident Fund. [Online] Available at: http://www.kwsp.gov.my/portal/about-epf/overview-of-the-epf [Accessed 9 September 2016].

Habib, S., 2007. The Star Online. [Online] Available at: http://www.thestar.com.my/news/nation/2007/05/27/countingon-the-nestegg/ [Accessed 13 September 2016].

Insurance, H., 2009. The Future of Retirement, s.l.: HSBC Insurance.

Investopedia, 2016. [Online] Available at: http://www.investopedia.com/terms/r/retirement.asp [Accessed 8 September 2016].

Malaysia, D. o. S., 2015. ABRIDGED LIFE TABLES, MALAYSIA, 2012 – 2015, s.l.: Department of Statistics Malaysia.

[/tw-toggle]

Prepared by Lee Hou Yin